2013 data endorses China collaboration on proposed co-productions

This Post has Comments Off on 2013 data endorses China collaboration on proposed co-productions

Chinese box office of more than $3.52bn in 2013 increased 27.5% on the previous year and received a boost from local fare, while foreign films are withering in the face of fierce competition, according to a new report from EntGroup Consulting.

The company’s China Film Industry Report 2013-2014 is its sixth annual study based on interviews, research and analysis on mainland China.

With the number of screens approaching 20,000 in 2013, local films saw a 54.3% year-on-year leap to gross $2.06bn. This accounted 58.6% of market share.

Foreign films grew a mere 2.3% last year, the lowest since 2007. Of 61 imported films released in mainland China, 34 were revenue-shared and 27 were on a flat-fee basis.

EntGroup says the 42% year-on-year decrease on the latter – which took only 8% of the annual box office – was due in part to prices being driven up by distributors snapping up films without a quota limit as well as difficulty in getting slots for the films in a competitive market place.

Overall the report says it “believes that the fundamental reason for the low growth of the market share of imported films is the lack of variety in recent imported films, many of which are sequels and re-releases, and heavily driven by special effects. In contrast, local films, such as So Young, Seeking Mr. Right and Tiny Times (pictured) are more diverse and relatable.”

It went on to say that despite having only one official China-US co-production, Man Of Tai Chi, films such as The Expendables 2, Cloud Atlas and Iron Man 3 all had involvement from Chinese companies and achieved global success. “We expect to see more and more collaborations between China and US productions on project and company levels,” the report said.

Market shares of China’s top 10 distributors in 2013

State-owned China Film Group and Huaxia Film, the only companies authorised to distribute foreign films on a revenue-sharing basis, remain the top two distributors, although their market shares have dropped since 2012 as a result of the lower performance of imported films.

1. China Film Group: 32.5%

2. Huaxia: 17.2%

3. Huayi Brothers: 12.5%

4. Enlight Pictures: 6.5%

5. Le Vision Pictures: 3.7%

6. Bona Film Group: 3.5%

7. Wanda Media: 1.8%

8. Edko: 1.5%

9. Beijing Union Pictures: 1.4%

10. SMG Pictures: 1.2%

P&A spend increases

P&A expenditures are on the rise with total marketing costs for China’s film industry in 2014 expected to reach $533m, growing almost four times in size since 2007.

In 2013, 22% of P&A spend was on in-theatre marketing and 20% on outdoor advertising. Traditional media advertising including TV took up 10% of marketing expenditure, while new media spend in China was only 5%, “but is expected to grow rapidly.”

Group-buying ticketing trends

Online group buying has become a major trend in China’s theatrical market. Group tickets sales accounted for 16.7% of total box office or $587.74m in 2013.

Third and fourth-tier cities were responsible for 53% of the group-buying sales. The rate is anticipated to rise even further as more online sites provide ticketing and seat-selecting services. Top film ticket group-buying sites include Dianping, Meituan and Nuomi.

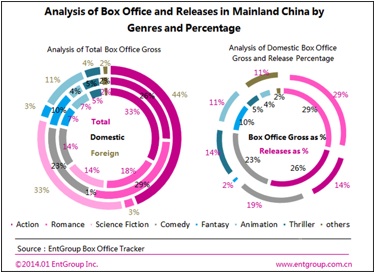

Genres

In 2013, action, romance, sci-fi and comedy were the four highest-grossing genres. EntGroup found that audiences went for romance and comedy the most for domestic films and action and sci-fi for foreign films.